60 Day Delinquencies Surpass Peak 2008 Numbers Easily

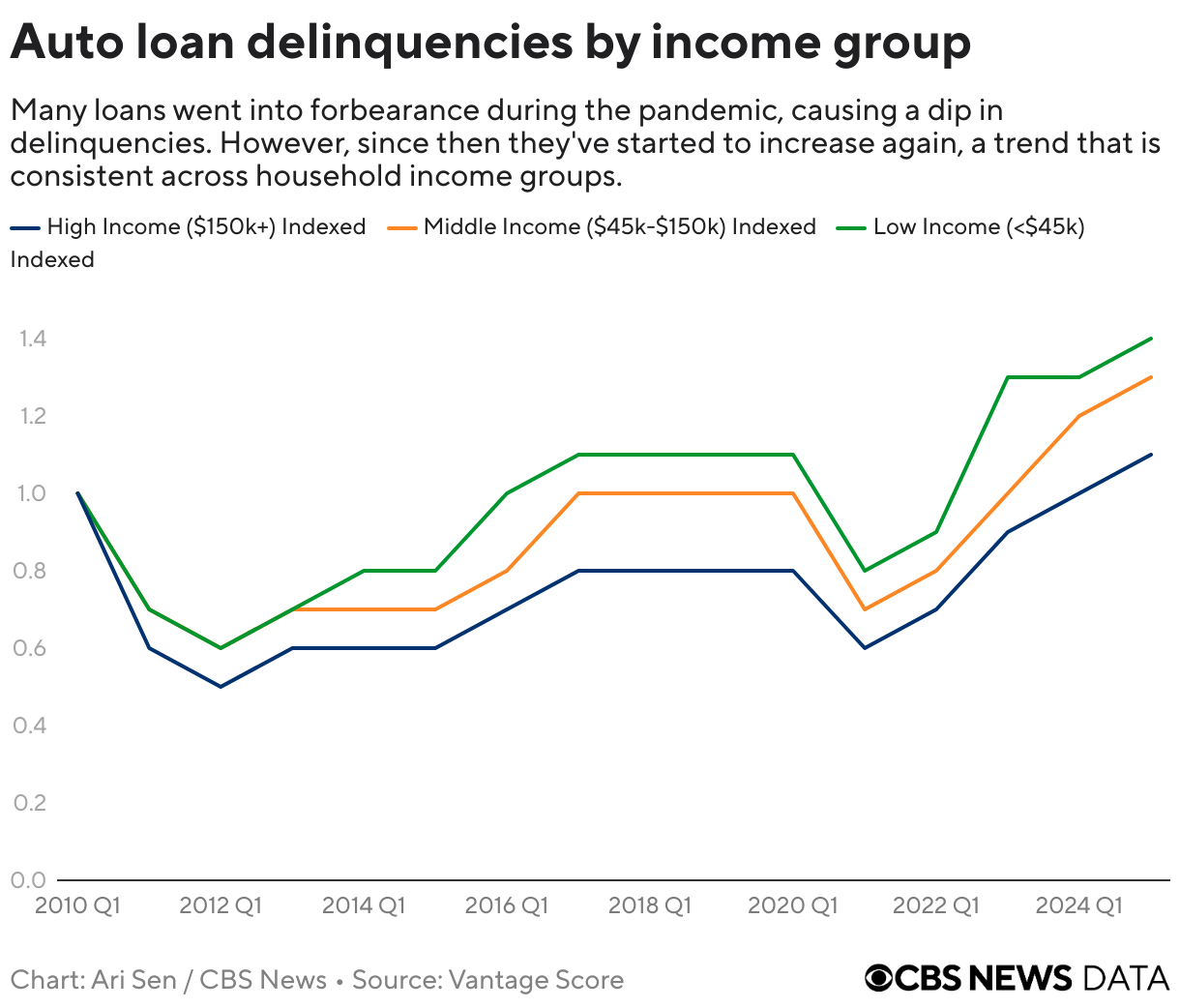

A growing share of subprime auto borrowers are falling behind on their vehicle payments, with delinquencies reaching levels not seen before. Data from Fitch Ratings’ ABS Index and Equifax shows that the percentage of subprime loans that are at least 60 days past due has climbed to 6.9%, surpassing the roughly 5% peak recorded during the 2008 financial crisis.

Financial pressure on these borrowers has been building since around 2022, as broader economic strain began to take hold. Many have been squeezed by high monthly car payments alongside rising living costs, including inflation, housing expenses, and existing debt. Employment instability, whether through job loss or reduced hours, has only made it harder for some to stay current.

For borrowers who fall two months or more behind, the situation can escalate quickly. Missed payments can lead to repossession if the account isn’t brought current, and for many, losing a vehicle can jeopardize their ability to get to work, creating a chain reaction of financial hardship. Delinquency also damages credit, leaving a negative mark that can remain for up to seven years. As a result, future borrowing becomes more expensive and, in some cases, unavailable.

Despite the pressure, communication with lenders remains one of the most practical steps a borrower can take. Being transparent about financial difficulties and providing a realistic timeline for repayment can sometimes open the door to temporary solutions or modified arrangements, particularly when hardship is tied to recent unemployment or reduced income.

From the lender’s perspective, delinquent accounts rarely end well. Once payments fall behind, lenders typically report the status to credit bureaus and may begin repossession proceedings. If the account continues to deteriorate, the loan can be written off as a loss, with the vehicle sold at auction in an attempt to recover part of the remaining balance.

The effects extend beyond individual borrowers and lenders. Rising delinquency rates are often viewed as a warning sign for the broader economy, signaling that consumers are under increasing financial strain. Because the credit impact lingers for years, borrowers may find it difficult to qualify for major purchases like a home long after the initial default.

Recent figures also show that total auto loan balances continue to grow, reaching $1.67 trillion in the fourth quarter of 2025 after a $12 billion increase. At the same time, new auto lending slowed slightly, with $181 billion in new loans reported during the quarter, down from $184 billion in the previous period.

Overall, the rise in serious delinquencies presents challenges across the board. Borrowers face long-term credit damage and the risk of losing essential transportation, while lenders are left managing losses, repossessions, and the uncertain recovery of outstanding balances.